Kazakhstan: What Trump’s New Tariffs Mean for Central Asia’s Role in Global Supply Chains

In April 2025, President Donald Trump imposed significant tariffs, including a 145% duty on many Chinese goods, dramatically altering global trade dynamics. Will Central Asia become more deeply integrated into China's economy, or will it successfully establish diverse partnerships with other international players?

KAZAKHSTAN

Raymond Puentes

5/15/20255 min read

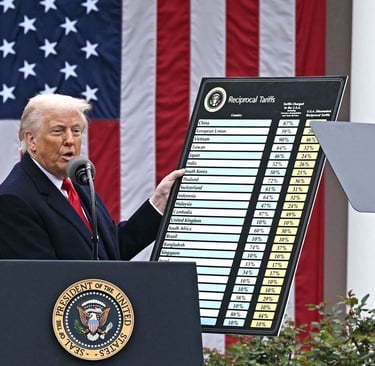

In April 2025, President Donald Trump implemented substantial tariffs. A base rate of 10% was applied to nearly all imports, and for a majority of Chinese goods, this rate escalated to 145%. These policies were enacted with the stated objectives of reducing United States reliance on foreign production and stimulating domestic industry. Nevertheless, their repercussions extended beyond the American economy. For Central Asia, a region characterized by significant natural resource endowments and a strategic geographical position connecting East and West, these new tariffs present both risks and potential opportunities. While the immediate economic effects on the region remained modest, the long-term implications are anticipated to be more substantial. Alterations in United States trade policy possess the capacity to influence Central Asia's integration into global production and logistics networks, as well as its diplomatic and economic engagements with key international actors, specifically China, the United States, and the European Union.

The direct impact of the new United States tariffs on Central Asia has been relatively limited, particularly for Kazakhstan, which holds the largest economy within the region. Kazakhstan is subject to the highest tariff rate in Central Asia, at 27%. Despite this, the primary export commodities of Kazakhstan, which include oil, uranium, and ferric salts, constitute a minor proportion of its total exports to the United States. It is important to acknowledge that approximately 92% of Kazakhstan's exports are presently exempt from these new tariffs, indicating that the energy and mineral sectors of the country are largely shielded from immediate adverse effects. As reported by sources such as Astana Times and Eurasianet, this exemption mitigates the direct impact of the tariffs on Kazakhstan. Given that the United States does not constitute a primary trading partner for Kazakhstan, disruptions to trade with the United States are expected to exert minimal influence. Other Central Asian nations, whose export volumes to the United States are even smaller, also remain largely insulated from the direct consequences of these tariffs.

While the immediate economic effects of the tariffs implemented by the Trump administration remain moderate, their long-term influence on the structure of global supply chains is becoming increasingly discernible. Global trade is experiencing heightened uncertainty, compelling corporations to reassess their logistics, defer orders, or undertake comprehensive restructuring of their supply chain configurations. Enterprises that historically relied upon "just-in-time" inventory management principles are particularly susceptible, as this model has demonstrated vulnerability under prevailing conditions.

Against this backdrop, new prospects are emerging for Central Asia. As companies globally endeavor to identify alternative suppliers to those in China, attention is increasingly directed toward a region endowed with substantial reserves of oil, natural gas, and mineral resources, in addition to its advantageous geographical location between East and West. In the context of the global impetus to diversify supply chains, Central Asia is positioned to attain a more prominent role within global logistics and trade networks. However, these opportunities are accompanied by considerable challenges. An increasing reliance on China as the principal economic partner introduces sensitivity to shifts in Chinese policy and domestic economic conditions. This is particularly pertinent given China's substantial investments in Central Asia's transport and energy infrastructure through the "One Belt, One Road" initiative. Such developments create a risk of excessive alignment with the interests of the People's Republic of China. Consequently, it is imperative for the nations of Central Asia to formulate a balanced and multi-vector development strategy to preserve flexibility and stability within the evolving global order.

The ongoing economic disengagement between the United States and China, driven by the tariffs imposed by the Trump administration, is projected to further intensify Central Asia's economic dependence upon China. As the United States implements tariffs on Chinese commodities, Chinese enterprises are likely to seek expanded operational engagement in Central Asia. This dynamic could result in increased Chinese investment and a greater volume of trade between China and Central Asia, particularly within the energy, infrastructure, and technology sectors. While this evolving relationship with China offers short-term stability for Central Asia, it simultaneously raises concerns regarding the region's long-term economic diversification. With China assuming an increasingly dominant position in the region, Central Asia may experience an augmented reliance on a singular external partner. This could potentially constrain the region's capacity to negotiate advantageous trade agreements with other major global powers and may undermine its efforts to broaden its economic foundation.

Despite the persistent challenge posed by dependence on China, Central Asia is presented with new opportunities for strengthening commercial ties with the European Union. In contrast to the rising protectionist tendencies in the United States, the European Union seeks to diminish its reliance on the economies of Russia and China. In this context, Central Asia, with its abundant energy resources and advantageous geographical position, can emerge as a pivotal partner for Europe, particularly in the pursuit of alternative energy supply sources to those from Russia and China. The European Global Gateway initiative, which aims to reinforce connections with other regions, provides Central Asia with an avenue to cultivate closer economic cooperation with the European Union. As noted by Astana Times, the region possesses the potential to play a significant role in the European Union's strategy to diversify supply chains, which could contribute to a reduction in dependence on China and the establishment of more balanced trade relationships. Within this framework, intra-regional cooperation is also gaining increasing importance. Illustrative examples include trilateral initiatives among Kyrgyzstan, Tajikistan, and Uzbekistan, which focus on energy development and infrastructure enhancement. Such actions contribute to the establishment of a more resilient regional economy, capable of adapting to global challenges, including economic instability originating from United States trade barriers.

The global progression toward the formation of regional trade blocs, such as ASEAN and BRICS, creates concrete opportunities for Central Asia. As nations and corporations seek new avenues to reduce reliance on established supply chains predominantly influenced by the United States and China, collaborative endeavors among neighboring states acquire particular significance. Central Asia's geographical location, positioned at the nexus of Europe and Asia, naturally positions it for participation in these developing trade platforms. The region can strategically leverage its natural resources, favorable geographical attributes, and active investments in infrastructure to assert itself as a significant global economic participant. By reinforcing ties with contiguous states and entering into regional trade agreements, Central Asia has the potential to mitigate its economic dependence on external powers and enhance its intrinsic stability within the international arena.

Despite the promising prospects for Central Asia, a multiplicity of risks remains. As indicated by the East Asian Forum, protracted trade tensions between the United States and China may ultimately precipitate a general deceleration of the global economy. This could result in a decline in commodity prices, a reduction in demand for natural resources, and an escalation of geopolitical instability, all of which would detrimentally affect the region's economy. For an extended period, Central Asia has adeptly maintained a delicate balance among major powers, preserving constructive relations with the United States, China, and Russia. However, this diplomatic equilibrium is experiencing increasing fragility. The augmented protectionism enacted by the United States and the expansion of China's influence, occurring concurrently with a perceived retreat of America from its role as a global trade leader, may impede the region's access to advantageous international commercial arrangements and restrict its economic opportunities.

The recent tariffs implemented by the Trump administration represent a significant juncture in international trade. While the direct economic consequences for Central Asia are presently limited, the long-term ramifications possess the capacity to reshape the region's position within global supply chains. As the region becomes increasingly integrated with China through commercial activities and infrastructure projects, it is imperative for Central Asia to concurrently pursue strategies for diversifying its partnerships and reducing its reliance on any singular external entity. Furthermore, the region must cultivate a capacity for adaptation to anticipated changes.

Central Asia possesses the capacity to capitalize on its advantageous geographical location and abundant natural resources to deepen its engagement in nascent regional trade blocs and strengthen its collaboration with the European Union. However, achieving this objective necessitates a careful equilibrium between its increasing dependence on China and a sustained openness to cooperation with a diverse array of global actors. The forthcoming years will be critical, as decisions made during this period will decisively shape Central Asia's future role within the global economy. Through the development of intra-regional cooperation, the expansion of its trade relationships, and the reinforcement of its position within global supply chains, Central Asia has an opportunity to evolve into a more stable and influential participant in international commerce.